Retail volume sales of European juice,considered in litres, declined by 1% in 2013. This weak performance continues a consistent downward trend in overall consumption of juice, with Europeans purchasing three fewer litres per person in 2013 than in 2003. Howard Telford, Analyst – Beverages, Euromonitor International

There are a number of negative trends applying pressure to the category. Juice can be a prohibitively expensive purchase in many parts of the continent, with higher prices of imported commodities (particularly Brazilian orange juice) reflected in the retail price on the shelf. In addition to price considerations, the category has a growing consumer perception problem. Despite widespread knowledge of the benefits of fruit consumption, juices are perceived by some parents as being too high in sugar for regular inclusion on the breakfast table. Furthermore, younger Europeans may view juice as unfashionable given the low emphasis on juice branding and roliferation of flavoured choices available in other impulse soft drinks categories.

Despite these external pressures, natural, higher value single-serve juice beverages could still provide a way forward for brand owners seeking to maintain profitability in a lower consumption environment.

Is juice just too expensive?

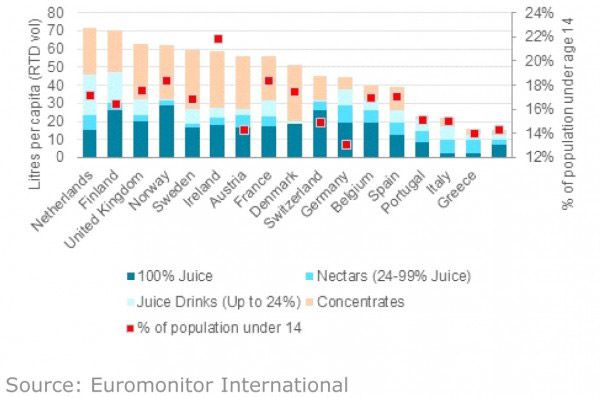

The type and value of juice (or fruit flavoured drinks) consumed in European markets is varied. The most affluent markets, including Switzerland and Scandinavia, are among the highest per capita consumers of 100% juice. In addition, the price of 100% juices in the richest European states can range from two to four times more expensive per litre than the Western European average. Prices have also been trending up in parts of the continent where consumer incomes have not, including Southern Europe. The simple inability of mainstream consumers to afford these natural, healthier juices can – to some extent – explain the poor performance of juice in the wider European market since 2006/07.

Cheaper, non-juice based fruit concentrates (liquid squash or powders) are a viable alternative to juices in some Northern European markets. As the chart below demonstrates, the product mix of ‘fruit’ based drinks (inclusive of both lower fruit content juice drinks and concentrates) varies considerably between European markets. Concentrates frequently lack the health benefits or natural ingredient claims of juices, but affordably replicate the sweet fruit taste of the drink and can be popular with children as a result. Occupying the middle ground, nectars (containing 24-99% juice) defend more market share in central Europe, primarily due to the popularity of German nectar manufacturers Eckes AG and Punica, with lower content juice drinks (less than 24%) also a less expensive choice for consumers in several markets.

Per capita sales of juice based drinks in Western Europe in 2013

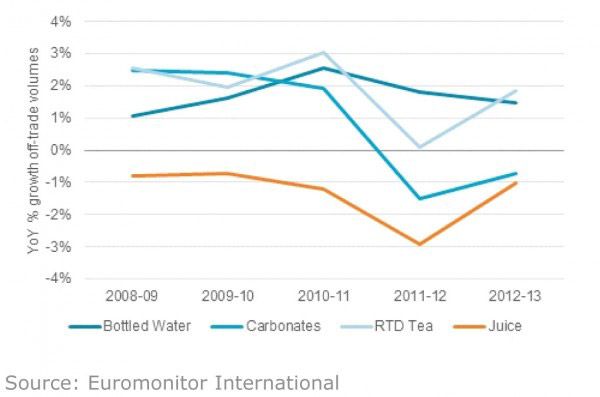

Retail volume growth of soft drinks in Western Europe

While no doubt important, the high price argument has definite limits in explaining the category’s longer term struggles. Declines in juice consumption preceded the 2008-09 downturn and have been more negatively impacted than other areas of soft drinks, such as water and carbonates. Over the last 5-years, European private label juice slightly underperformed the category in terms of value sales growth. While the market may be entering a slower rate of total juice intake, some branded players are succeeding in driving more value per bottle by reducing package sizes and emphasising the wellness properties of the product.

While no doubt important, the high price argument has definite limits in explaining the category’s longer term struggles. Declines in juice consumption preceded the 2008-09 downturn and have been more negatively impacted than other areas of soft drinks, such as water and carbonates. Over the last 5-years, European private label juice slightly underperformed the category in terms of value sales growth. While the market may be entering a slower rate of total juice intake, some branded players are succeeding in driving more value per bottle by reducing package sizes and emphasising the wellness properties of the product.

Reaching children and adults through better branding and packaging

The Netherlands is the second largest per capita market for juice consumption and the number one market for overall fruit drink consumption when factoring in RTD concentrate volume. It should come as no surprise that recent academic studies have demonstrated that Dutch children have among the highest daily consumption (380 ml) of European states. Maintaining young consumers remains vitally important to the success of the juice category.

The French juice drink Oasis (Orangina-Schweppes) grew retail volume sales by 19% over the last three years through a cohesive marketing campaign which made a concerted effort to engage their younger consumers and distinguish their product from a wide range of competition (including low-priced private label). Oasis employed TV advertising, cartoon fruit icons and a robust social media presence. The brand have 3.2 million Facebook followers- an extremely high number for a juice brand (Pepsi’s Tropicana, by way of comparison, have just over 1 million followers). A successful focus on product branding has enabled the Oasis brand to better communicate its health properties to consumers in a high profile but light hearted way, bucking the downward trend in the category. DubbelFrisss, a successful Dutch brand of juice, have also succeeded in reaching young consumers through a mix of unusual, eclectic flavours (such as kiwi and pineapple or lemon and grape) and a similarly off-beat marketing approach.

At the opposite end of the consumer spectrum, a sustained interest in superfruits, premium juices and the functional properties of juices may succeed in driving consumption among adult consumers. Proviva – a Swedish and Finnish juice brand – achieved 40% volume growth over the same 2010-13 period through the marketing of a probiotic juice. Marketing for the brand is wellness focused and premium priced.

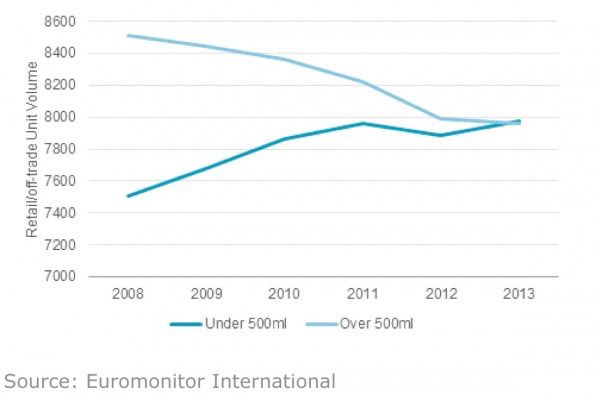

Retail unit volume of fruit/vegetable juice packaging

The above chart demonstrates another avenue for improving value per purchase. When examining unit volumes of juice packaging, it becomes apparent that smaller pack sizes - impulse retail purchases - have dramatically outperformed larger, take-home juices over the forecast period. While total liquid volume has declined, the smaller, much higher value pack sizes have gained share at the expense of family pack sizes. Smaller package sizes can provide higher profit margins for brand owners while maintaining reasonable shelf prices.

The above chart demonstrates another avenue for improving value per purchase. When examining unit volumes of juice packaging, it becomes apparent that smaller pack sizes - impulse retail purchases - have dramatically outperformed larger, take-home juices over the forecast period. While total liquid volume has declined, the smaller, much higher value pack sizes have gained share at the expense of family pack sizes. Smaller package sizes can provide higher profit margins for brand owners while maintaining reasonable shelf prices.

Keys to European growth

The juice industry will make a mistake in waiting for a recovering European economy to provide the impetus to rebounding household consumption. Consumer factors will also be an important piece of the puzzle. The successful brands in European juice have bucked the trend by responding to this fact. While prices have increased due to higher commodity costs, there has also been a trend down from larger bottles to single serve purchases, driving higher value sales per litre.

Impulse, on-the-go purchases and on-premise consumption will be keys to revival in the category. Smaller packages and serving sizes can allow consumers to exercise control over sugar intake and calories while maintaining the healthful properties of juice or prominent functional elements. Over the forecast period, there should be more emphasis from juice brands in the impulse soft drinks segment, where shelf space is diversifying and consumer tastes expanding. Less product mix and marketing attention should be spent on the family size carton, where volume consumption has dipped the most significantly over the review period.

Winning brands in high consumption markets – such as Scandinavia and the Netherlands – have been adept at clearly conveying the functional elements of their product to adults. Other brands (including Oasis) have appealed to children and parents through a fun brand message supported by the health properties of fruit juice ingredients. [MS1] Fruit juice brands across the continent should seek to emulate these successful approaches. While the overall juice category is expected to remain flat over the forecast period, off-trade value sales of not from concentrate 100% juices are forecast to increase by 9% in constant value terms through 2018. Consumers will choose juice products with legitimate ‘allnatural’ claims, accepting the price premium over overly processed, artificial juices.

For further insights contact Howard Telford at howard.telford@euromonitorintl.com

Source: Howard Telford, Analyst – Beverages, Euromonitor International.

Published: 2014-03-14